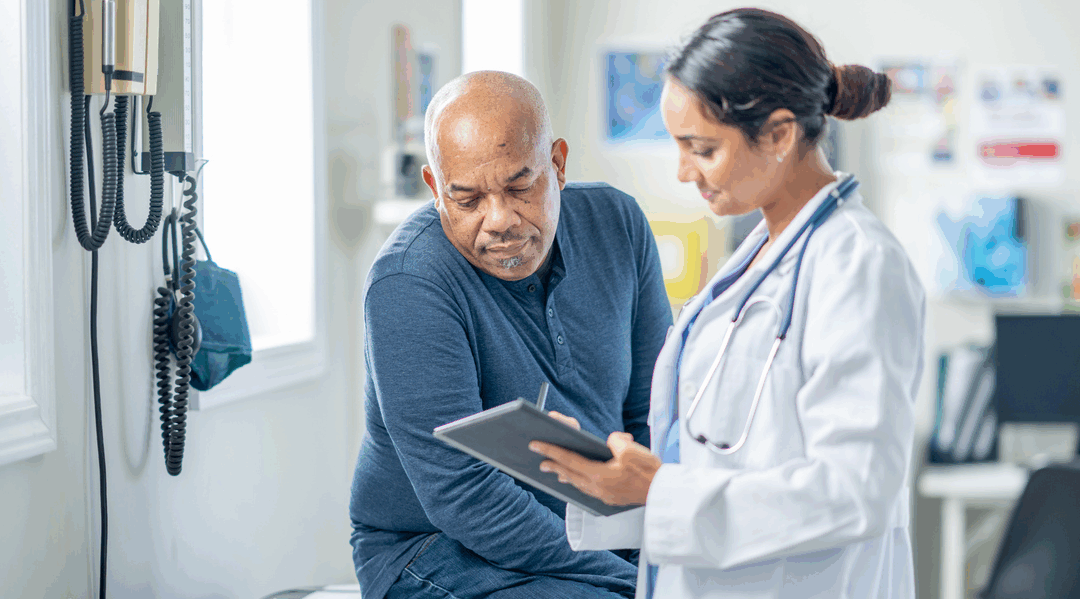

As cancer rates rise among working adults, treatment has become one of the fastest-rising expenses in employer-sponsored health plans, according to a new survey.

The survey by the International Foundation of Employee Benefit Plans (IFEBP) found that 86% of employers have seen their cancer care spending increase over the past year, with a median rise of 11%, making it one of the most significant contributors to overall health care cost growth.

As more employees get diagnosed with cancer, which in turn increases the cost of care for employers, they are increasingly turning to strategies that direct plan members to high-quality, cost-efficient providers and care facilities.

What’s driving the trend

Employers report that cancer-related costs are increasing due to a mix of:

Expensive specialty drugs — Many of the newest cancer drugs can cost $20,000 to $40,000 per month, while gene and cell therapies can top $1 million per course. Even with negotiated network discounts, the compounding cost of these treatments is straining plan budgets.

New treatment technologies — New high-cost therapies like immunotherapies and gene-based treatments are regularly coming on line.

A higher number of working-age adults being diagnosed with cancer — New cancer diagnoses are expected to exceed 2 million cases in 2025, with rising rates among women under 50 and cancers such as colorectal, breast and cervical appearing more often in younger age groups.

More people are surviving cancer — Employees and their dependents are entering treatment phases earlier and remaining in survivorship programs longer, adding sustained costs for employers.

How employers are responding

Employers are increasingly turning to steerage techniques that direct plan members to high-quality, cost-efficient providers and care pathways. According to IFEBP, the most common approaches include:

Nurse navigators (63%) to help employees coordinate complex care.

Second-opinion programs (58%) to validate treatment plans.

Centers of excellence (42%), which offer bundled, value-based pricing.

Treatment center networks (24%) and virtual care clinic vendors (18%).

Value-based contracts (17%) and point-of-care testing (15%).

Among employers using these strategies, the primary goals are:

Improving outcomes (66%),

Offering personalized support (59%) and

Negotiating lower prices (33%).

Nearly a third is experimenting with alternative payment models such as shared-savings or bundled-rate arrangements that tie reimbursement to results rather than the volume of care.

Prevention and early detection

Experts say early detection offers the greatest potential to control both costs and outcomes. However, only about half of employees receive annual preventive care, and a significant portion of catastrophic cancer claims is linked to individuals who skipped routine screenings.

Employers can help by:

Promoting annual preventive exams and age-appropriate cancer screenings.

Covering or incentivizing genetic and biomarker testing for at-risk employees.

Incorporating AI-assisted diagnostics and at-home testing options for early detection.

Providing educational campaigns on modifiable risk factors such as smoking, obesity and inactivity.

To manage this, benefit professionals are urged to take a comprehensive, life-cycle approach from prevention and early screening to treatment navigation and survivorship care. As Julie Stich, IFEBP vice president of content, noted, employers must “offer the most effective cancer care treatments while also exploring cost-control techniques.”

With health insurance costs continuing to climb, many employers are finding that standard medical coverage alone doesn’t offer enough financial protection for their staff.

Rising deductibles, higher out-of-pocket maximums and the soaring cost of care are pushing workers to look for other ways to fill the gaps. Employers can step in to meet that need with voluntary benefits.

Once considered optional add-ons, voluntary benefits such as accident, hospital indemnity, critical illness, group life, dental and vision insurance are increasingly becoming essential parts of a well-rounded benefits package. Wellness programs, employee assistance plans and financial counseling options are also now viewed as integral to overall well-being.

A shift in expectations

Prudential’s “2025 Benefits and Beyond” study found that nearly a quarter of employees expect these voluntary benefits to be included as part of a modern workplace offering. But often, employers are not providing the benefits that employees say they need. The poll found that 86% of employers say their benefits are modern, but only 59% of employees agree.

This discrepancy has started to resonate with employers. As a result, 70% of employers plan to make changes to their benefits offerings within the next two years, with 22% expecting significant overhauls.

Employees say their biggest concerns are:

Saving for retirement (45%),

Covering everyday expenses (44%),

Paying for housing (29%), and

Simply making it from paycheck to paycheck (26%).

When a single medical event can upend financial stability, benefits that offer supplemental protection can provide an important financial backstop and save an employee from financial disaster.

Why voluntary benefits matter now

Voluntary benefits provide cost-effective coverage options that protect employees from the unexpected.

For example:

Accident, critical illness and hospital indemnity policies help offset out-of-pocket costs that major medical insurance doesn’t cover, such as co-pays, deductibles, transportation, lodging and lost income during recovery.

Dental and vision plans promote preventive care that can reduce larger medical costs over time.

Wellness and mental health programs, another key element of today’s voluntary benefits landscape, help employees manage stress and anxiety that affect productivity and retention. (In Prudential’s research, 63% of employees said they have mental health concerns for themselves or a family member, yet only about the same share feels their benefits help them manage overall well-being.)

Benefits for both sides

Expanding voluntary benefit offerings and ensuring you have the benefits your employees really want support recruitment and retention while containing costs.

Because these plans are typically employee-paid through payroll deduction, they add value without significantly raising the employer’s benefit budget. Employers also gain a competitive advantage in a labor market where workers expect more comprehensive protection and well-being support.

Employees gain access to affordable coverage that helps them manage risk and avoid financial hardship. For many, paying a few extra dollars per paycheck for supplemental coverage can prevent a small setback from becoming a financial crisis.

With employers bracing for another steep rise in health care expenses, many are preparing “disruptive” changes, according to a new report.

Employers surveyed for the “WTW 2025 Best Practices in Healthcare Survey” said they anticipate their health care costs will increase by 9% in 2026. They told researchers they can’t absorb the increases or pass them on in full to employees, and instead hope to chip away at costs through a multi-pronged approach.

Since your are likely experiencing cost pressures as well, here’s a look at what your peers are experiencing and doing about it.

Where employers will focus

Managing vendor contracts — Survey results show 46% of employers are actively evaluating vendor performance.

Pharmacy benefit managers are under particular scrutiny, with three-quarters of employers either bidding out or planning to rebid their PBM. Many are also exploring more transparent, pass-through contract models.

Conducting audits — One-third of employers already conduct medical claims audits, and nearly half plan to add them. Another 22% have reviewed prior authorization or out-of-network payments, with 34% planning to.

These audits help uncover overpayments, billing errors or inappropriate authorizations. By increasing oversight, employers can identify waste, enforce contract terms and make sure vendor processes align with plan rules.

Preventing overutilization and abuse — Unchecked use of services remains a top cost driver, especially for specialty drugs, imaging and inpatient procedures.

Employers are taking a closer look at utilization controls, including stricter prior authorization, step therapy for high-cost drugs and site-of-care management to steer members toward lower-cost outpatient settings.

Note: Step therapy involves trying other lower-cost methods first, such as other proven medicines that aren’t as costly as new medications.

Alternative plan designs — Currently used by 41% of companies, alternative plan designs are expected to grow rapidly, with adoption potentially reaching 87% within two years.

These designs may include:

Tiered or narrow networks,

Transparent cost tools, and

High-performance primary care models.

Employers are also using technology and enhanced navigation to guide employees when choosing providers. By structuring benefits to reward use of cost-effective, high-quality providers, employers told WTW they hope to chip away at growing costs while improving the employee experience.

The takeaway

If you are are concerned about rate hikes, talk to us about steps you can take to get a better handle on your health plan by incorporating some of the steps listed above.

When it comes to pharmacy benefit management, not all PBMs are created equal. Many traditional PBMs rely on opaque pricing models, hidden rebates, and misaligned incentives that can drive costs up instead of bringing them down. For benefits consultants, asking the right questions up front is key to ensuring transparency and delivering measurable savings.

Below is a checklist of essential questions every benefits consultant should ask a prospective PBM, along with red flags and differentiators to look for.

How is your pricing structured?

Why it matters: Traditional PBMs often profit from spread pricing and rebate arrangements that aren’t in the client’s best interest.

Red flag: If the PBM avoids explaining how they make money, chances are the incentives are misaligned.

What to look for: A pass-through pricing model with full transparency. At US-Rx Care, we don’t profit from rebates; we align savings directly with the plan sponsor.

Can you guarantee clinical savings, not just discounts?

Why it matters: Discounts sound good, but they don’t always translate into lower net costs. Without effective clinical management, “discounted” drugs are only solving for one piece of the puzzle.

Red flag: A PBM that only talks about discounts without showing outcomes data.

What to look for: Evidence-based clinical oversight that ensures patients are on the right drug at the right time, preventing unnecessary spend.

How do you handle specialty medications?

Why it matters: Specialty drugs represent less than 2% of prescriptions but more than 50% of drug spend. This is where PBMs often inflate margins.

Red flag: Limited transparency around specialty sourcing and pricing.

What to look for: Programs that ensure clinical appropriateness and offer alternative sourcing strategies. US-Rx Care consistently delivers significant savings on specialty medications without reducing access or quality.

What level of transparency do you provide?

Why it matters: A PBM should be a partner, not a unknown variable. Without visibility, consultants and plan sponsors can’t validate true performance.

Red flag: Reporting that’s overly complicated or excludes certain fees, rebates, or data.

What to look for: Full transparency in contracts, reporting, and outcomes. US-Rx Care provides clear, auditable reports so consultants can demonstrate value with confidence.

How do you align with fiduciary responsibility?

Why it matters: Plan sponsors have a fiduciary duty to act in the best interest of their members. A PBM that prioritizes its own profits puts employers at risk.

Red flag: Any PBM that claims savings but can’t demonstrate alignment with ERISA requirements.

What to look for: Fiduciary-focused solutions that ensure plan sponsors meet their obligations. US-Rx Care contracts are built to protect both the plan and its members.

Key Takeaway for Consultants

A PBM should work for the client, keeping their best interests, and those of the members, at the forefront. By asking these critical questions, benefits consultants can uncover red flags and position themselves as trusted advisors who deliver real value.

We’ve built our model around transparency, fiduciary alignment, and clinically driven savings. The result? Lower costs, better outcomes, and confidence that your PBM is truly on your side.

Discover how US-Rx Care can deliver measurable savings and transparency for you. Connect with us today at usrxcare.com/contact.

If you view annual open enrollment as a simple box-checking exercise, you’re likely missing out on helping your staff get the most out of the benefits you provide.

Instead, if you approach open enrollment as a chance to strengthen employee engagement, control costs and help your workforce understand the full value of your benefits program, you’ll likely boost participation and satisfaction among your staff.

With health care costs rising, financial stress growing and multiple generations in the workforce, employers need to approach open enrollment as a strategic initiative rather than a compliance deadline. This is more important than ever given rapidly rising premiums that will affect both your organization and your staff.

Here are seven best practices to keep in mind:

1. Focus on generational needs

Employees at different life stages want different things from their benefits:

Gen Z often looks for flexibility and mental health resources.

Millennials focus on balancing family and financial security.

Gen X may prioritize saving for retirement.

Baby boomers often care most about health coverage and stability.

Tailoring communication and plan design to these priorities can boost engagement across the board.

2. Avoid two big mistakes

Employers often make two main mistakes you’ll want to avoid:

Overloading employees with materials and presentations full of jargon. This is a sure way to lose their interest.

Failing to provide the necessary support to help them make decisions about which plan to choose.

Keep messaging simple, practical and easy to understand. Provide comparison tools, FAQs and one-on-one support when possible so employees don’t feel lost.

3. Do what works

Personalize your benefits education by providing tailored communications for each generation in your workplace. Use multiple communication channels like text messages, e-mail, print materials and the company intranet.

Help employees understand how benefits support their physical and mental health as well as their long-term financial security.

4. Provide year-round benefits communications

Regular benefits communications throughout the year can make open enrollment much easier for your staff. Some ideas include:

Reminders about their benefits and how they can use them.

Micro-learning tools, which deliver training in short, focused lessons through platforms like mobile devices and learning management systems. These tools improve knowledge retention and boost engagement.

Fact sheets on the benefits they are eligible for to help them discover options they may not know about but would like to have.

5. Plan ahead

The most effective open enrollment strategies are carefully planned. As part of this process:

Review last year’s open enrollment results.

Set clear goals.

Segment your employee population to identify gaps and opportunities.

Track outcomes so you can improve each year.

6. Consider new tech

Digital decision-support tools, including AI-driven platforms, can simplify open enrollment by providing employees with personalized plan recommendations.

These tools also give HR teams valuable data on employee behavior and preferences, which can guide future plan design and communication.

7. Play up the benefits of benefits

Frame your offerings as a stabilizing force. Emphasize that benefits provide consistency and protection when life is unpredictable, giving employees confidence that their health, income and families are supported no matter the circumstances.

By framing benefits as a safety net, you can show your staff how these programs help provide stability in daily life.

Takeaway

Employers who approach open enrollment strategically — with a focus on affordability, engagement and education — can turn a required process into a competitive advantage.

By meeting employees where they are and communicating clearly, you reinforce the value of your benefits program and strengthen trust within your organization.

The Departments of Labor, Treasury and Health and Human Services announced that they will no longer enforce a 2024 rule limiting short-term health insurance to three months.

The decision leaves the door open for insurers to once again issue these policies for up to three years, as they were permitted under rules implemented during President Trump’s first term. The agencies emphasized that the rule itself remains in place but said they “do not intend to prioritize enforcement actions” against plans that exceed the Biden-era restrictions.

Officials also signaled that they are considering further changes to how these policies are regulated, though no timeline was outlined.

A shifting regulatory landscape

Short-term health plans have been a political football across three administrations.

In 2016, the Obama administration finalized a rule limiting the plans to three months, calling them temporary stopgaps.

In 2018, Trump extended the maximum duration to one year and allowed renewals up to three years. Sales surged after that change.

In 2024, the Biden administration rolled back the expansion, capping the plans at three months with no more than four months of total coverage including renewals.

With the latest move, enforcement of that cap is on hold, giving insurers room to once again sell longer-duration plans.

How the plans work

Short-term policies are typically less expensive than Affordable Care Act-compliant coverage because they are not subject to ACA rules. These plans were originally envisioned as a bridge between jobs or coverage transitions, not as long-term solutions.

For smaller employers that are not subject to the ACA’s mandate to offer affordable health coverage, short-term policies could be an option for workers seeking lower-cost alternatives.

But because short-term coverage is distinct from comprehensive health insurance, employers evaluating whether to steer workers toward these plans should understand the trade-offs:

Preexisting conditions can be excluded.

Coverage can be denied based on health history.

Annual and lifetime benefit caps may apply.

Preventive care, maternity care and mental health services are often not included.

No protection under ACA consumer safeguards such as the No Surprises Act or parity requirements for mental health.

Short-term plans can also exclude certain benefits that ACA plans are required to cover.

State restrictions

While federal regulators are stepping back, states still control whether these plans can be sold within their borders.

Fourteen states plus the District of Columbia bar them altogether, including California, New York and New Jersey. Other states allow them but impose strict duration limits or conditions that make them impractical for insurers to offer.

Potential changes ahead

The agencies noted they are considering additional adjustments to the rules governing short-term plans. Possible areas of change could include:

Redefining the maximum duration,

Revisiting required consumer disclosures,

Imposing new standards for renewals, and

Allowing for stacking of policies.

Any proposed rulemaking would undergo a public comment process before becoming final.

Takeaway for employers

The federal decision creates uncertainty in the market, with enforcement discretion now favoring longer short-term policies but no clear timeline on new rules.

Employers with fewer than 50 employees may see these plans as a possible option for workers, but larger employers remain bound by ACA requirements to provide affordable, minimum-value coverage.

As the agencies move toward potential new regulations, employers should monitor developments closely and weigh the risks and limitations of short-term health plans before considering them as part of a benefits strategy.