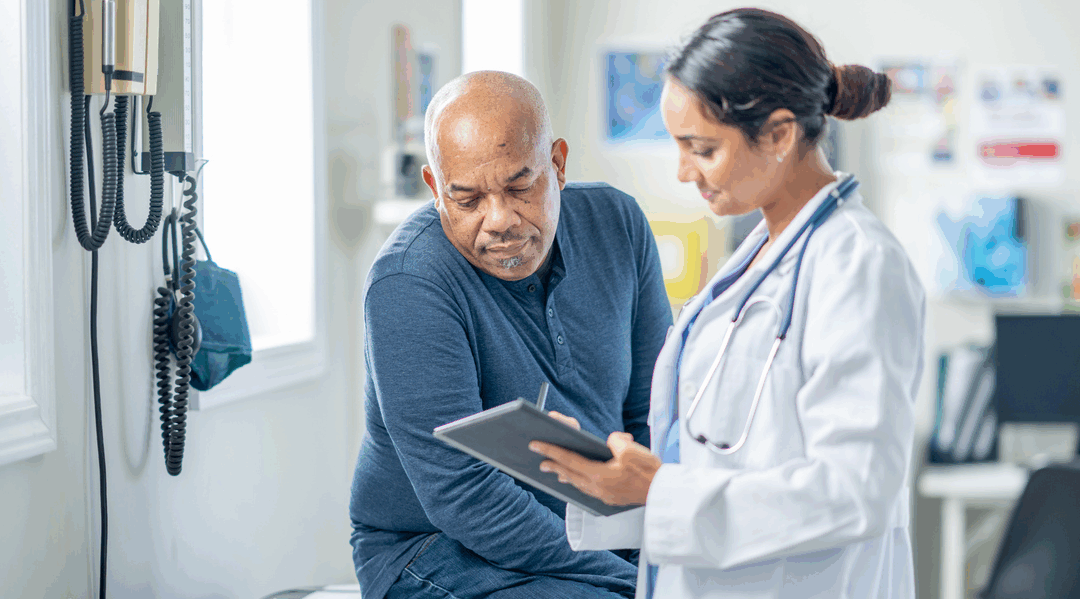

Choosing the right dental insurance plan for your employees is always filled with compromises and difficult decisions, no matter if this is the first time you offer a dental plan at your company or you are just revising the benefits currently on offer.

The process becomes even more difficult when you look into the variety of options and types of dental benefits there are today. Here’s some information to help simplify the situation:

Coverage types

There are three basic types of dental coverage employers typically offer:

Indemnity plan — These fee-for-service style plans are the most common type. They require employees to pay monthly premiums to the insurance company, which agrees to reimburse dentist offices for the costs of the services provided.

What makes these plans so popular is the freedom that covered individuals have in choosing their own dentist. Fee-for-service plans cost more than other plans, but many people are willing to pay more to retain the ability to choose their own practitioner.

Preferred provider organization — PPO dental plans are less expensive than indemnity plans, while still providing a large pool of dentists to choose from. Individuals covered under PPO plans are given the choice of receiving care from any provider within the plan’s dentist network or choosing a non-network dentist and paying a little more in out-of-pocket expenses.

Dental health maintenance organization — A DHMO is the least expensive type of plan. Covered individuals are given an even smaller pool of in-network dentists and may not receive coverage if treated at a non-network facility. DHMOs are able to cut costs by placing a strong focus on preventative care and by offering a selective number of dentists to choose from.

Services covered

Besides choosing one of the three styles of dental insurance, the employer must decide on a benefits program that covers specific services. For example, some plans are comprehensive and cover everything from preventative care to major procedures, while others only cover preventative services.

In dental terms, preventative care refers to semi-annual check-ups and cleanings, yearly x-rays, and fluoride treatments and sealants for children covered under the plan. Basic dental care would refer to basic oral surgeries and restoration procedures. Major dental care refers to root canals, extractions, crowns, prosthetics and advanced surgeries.

Dental plans can also be customized to include services like orthodontics and cosmetic dentistry procedures through the use of riders and options. For a small fee, supplemental services can be added to bulk up basic coverage plans.

The takeaway

When facing such an important decision, numerous factors play into your choice. You must juggle the wants and needs of your employees with the cost and range of each plan. Is it better to have choices or to pay less in premiums?

The more communication you have with your staff, the better you will understand how to formulate a dental insurance plan that meets their expectations.

By promoting good oral health within the workplace and through a benefits program, you will be doing a great service to your employees and your business.

The oldest Gen Z workers and youngest Millennials who are just entering the workforce face a steep learning curve when selecting group health plans coverage and are increasingly turning to apps, the internet and family for advice, according to a new report.

The survey by Justworks and The Harris Poll found that the youngest workers experience the greatest stress during open enrollment, lean heavily on AI tools and social media for guidance and rarely ask their employer’s HR team for help.

For employers, the findings highlight a widening generational divide in how workers research, understand and engage with health benefits. Employers will need to account for this new generation in their communications and support services.

Research habits are changing

Despite their concerns, nearly 60% of Gen Zers spend an hour or less reviewing benefits.

Their methods also differ sharply from older generations.

62% have used AI tools, including ChatGPT, to help interpret plans.

30% turn to TikTok and other social platforms for advice.

Younger Gen Zers are more likely to call a parent than consult HR.

11% ask a benefits manager for help.

This contrasts with Millennials, who rely more on Google and Gen Xers and Boomers, who tend to use employer resources. The report also found that zillennials value quick, tech-first explanations and tools that compare plans in simple terms.

Lack of understanding

According to the survey, about 26% of Gen Z workers say affordability is their biggest concern when choosing a plan. That angst is compounded by the fact that many are making these decisions for the first time as they roll off their parents’ coverage.

Here’s what the survey found about the oldest Gen Zers and youngest Millennials:

52% say they don’t know much about choosing an insurance plan because they’ve never had to do it before.

20% say they aren’t confident about picking a suitable plan.

44% don’t put much thought into the process.

The oldest Gen Zers and youngest Millennials also report uncertainty about which questions to ask during open enrollment or who to approach for answers.

This further pushes them toward AI, online communities and social media, where health insurance advice is often incomplete, biased or incorrect.

What employers can do

As more Gen Zers enter the workforce, they will likely have the same habits as those identified in the survey. The stakes are even higher as rising medical costs make it more important for workers to choose appropriate plans.

The survey suggests several steps employers can take to help the youngest workers make better decisions:

Provide short, simple explainers rather than long benefits guides.

Use clear comparisons that highlight key differences between plans.

Offer examples tied to situations younger workers understand, such as renters or auto insurance.

Ask workers directly whether they are consulting TikTok, Instagram or AI tools for guidance and what kind of advice they’ve gotten.

Correct misinformation before open enrollment begins.

Encourage employees to bring questions to HR instead of relying solely on outside sources.

Because social platforms contain a significant amount of inaccurate benefits content, it’s useful for HR teams to check in early and clarify what is and isn’t true. Employers may also want to incorporate AI-enabled tools into their own communication strategy, giving staff a trusted version of technology they already use.

The oldest members of Gen Z are signaling that they want simpler information, faster answers and digital guidance that matches how they already learn. Employers that adjust their communication to meet these expectations can help younger workers feel more confident in their choices — and reduce costly mistakes during open enrollment.

New federal guidance announced Oct. 16, 2025, could make it easier for companies to add or expand fertility support for workers without having to fold it into their major medical plans.

The guidance, a new set of FAQs issued by the Departments of Labor, Health and Human Services and Treasury, spells out how infertility benefits like in vitro fertilization and hormone therapy can qualify as “excepted benefits,” a category of coverage that’s not subject to Affordable Care Act mandates. The guidance was in response to an executive order issued by President Trump in February 2025.

Under the ACA, most employer health plans must follow strict coverage and reporting rules. But certain benefits — such as dental, vision, FSAs, HRAs, EAPs and hospital indemnity plans — are “excepted,” meaning they’re exempt from the ACA’s mandates on preventive care, annual dollar limits and other requirements.

Three options

Under the new guidance, employers have three ways to structure fertility benefit coverage:

1. Separate, insured fertility policy — Employers can now buy a fully insured policy that covers infertility care as its own benefit. To qualify as an excepted benefit, the policy must:

Be issued under a separate insurance contract.

Not coordinate with the company’s main health plan.

Pay benefits regardless of what the health plan covers.

This lets employers extend fertility coverage to all workers, even those not enrolled in the medical plan. Self-funded programs don’t qualify under this option.

2. Excepted benefit HRA — An employer could reimburse out-of-pocket fertility expenses through an “excepted benefit” HRA if it meets federal limits. To qualify, the HRA:

Must be offered alongside a traditional group health plan.

Can reimburse up to $2,200 in 2026 (indexed annually).

Can’t reimburse insurance premiums.

Must be offered on the same terms to similarly situated employees.

It’s a smaller-scale solution but can help offset costs for staff pursuing fertility treatment.

3. Employee assistance program — Employers can use an EAP to offer coaching or navigator services that help workers understand their fertility options or find providers. The EAP cannot provide “significant” medical care or be tied to the main health plan, and participation must be free and voluntary.

This option doesn’t pay for treatment but adds support for staff exploring fertility services.

Examples of fertility benefits

Depending on the setup and insurer, fertility coverage may include:

Diagnostic testing and consultations

Fertility drugs and hormone therapy

Procedures such as in vitro fertilization or intrauterine insemination

Egg, sperm or embryo storage

Donor services or gestational carrier expenses

Coaching, navigation or second-opinion services

Employers that already cover fertility care under their medical plans can continue to do so, but the new guidance gives more flexibility for those wanting to offer coverage to a broader workforce.

Takeaway

The new FAQs are informal guidance that expands on existing rules rather than creating new legal avenues for fertility coverage.

The agencies also stated they intend to propose regulations that could add more ways to offer infertility benefits as limited excepted benefits and may revisit standards for supplemental coverage.

If you offer or plan to offer fertility benefits, be alert for upcoming rulemaking and review designs with counsel to keep your offerings ACA-exempt and compliant.

A new survey from America’s Health Insurance Plans (AHIP) and the Blue Cross Blue Shield Association (BCBSA) is raising alarms about widespread abuse of the federal Independent Dispute Resolution process set up under the No Surprises Act.

According to the findings, nearly 40% of disputes filed through the system in 2024 (the year the law took effect) were ineligible, yet many still advanced through arbitration, forcing employers and health plans to pay unnecessary or inflated claims. Many of these claims are driven by private equity-backed health care providers and not individual health plan enrollees, according to the survey.

According to Kim Keck, president and CEO of BCBSA, the volume of dispute resolution cases has exceeded expectations and is clogging up the system. Many decisions are made despite evidence that the claim is ineligible for compensation.

What the survey found

The survey, which polled health plans covering 154 million Americans, found that:

40% of all disputes were identified by insurers as ineligible, including 45% of nonemergency service disputes.

Only 17% were ultimately deemed ineligible by the federal arbitration entities, meaning more than half of improper cases still resulted in binding payment determinations. This suggests that the referees in the IDR system are failing to identify a large volume of ineligible disputes submitted by providers.

20 million claims were filed in 2024, with emergency services making up about 61% of the total.

Air ambulance claims, though fewer than 1% of submissions, were the most likely to reach arbitration and involved high-dollar payouts.

Bright spots

While the survey identified potential abuse in the system, it also found evidence that it works in legitimate cases:

In 2024, nearly 20 million health care claims met the criteria for federal surprise billing protections, meaning nearly 20 million surprise bills were prevented in 2024.

Three out of four claims were paid without further dispute when providers accepted the plan’s initial payment.

Once arbitration decisions are issued, plans pay nearly three-quarters of arbitration awards within 30 days; 41% were paid in just 15 days.

When delays occurred for qualified IDR items or services, they were most often due to provider submission errors (e.g., wrong contact info, missing details) or processing challenges stemming from the very high volume of IDR cases.

The crux

While the No Surprises Act has successfully shielded employees from unexpected medical bills, the volume of ineligible disputes now clogging the system is driving claims costs.

Arbitrators often side with providers, leading to payments that far exceed in-network rates. As those costs cascade through plan spending, premiums and overall claim costs rise, affecting employer budgets and employee contributions alike.

AHIP and BCBSA said the current system lacks a workable appeal process, leaving plans no avenue to challenge decisions even when the underlying dispute should never have qualified.

The two groups are urging federal regulators to tighten oversight, clarify eligibility rules and impose stronger screening to prevent improper cases from moving forward.

They also called for “realigned incentives” so that independent dispute resolution entities are not rewarded for pushing unnecessary claims through arbitration.

Takeaway

For employers, the survey highlights how a well-intentioned law meant to protect patients has, in practice, created a potentially costly loophole.

Until regulators reform the system, arbitration under the No Surprises Act may continue to inflate claims costs and premiums, even for cases that never should have been disputed.

Staying in the same plan after year can be a waste of money if someone is in the wrong plan for them. And not understanding benefits can lead to wasted money as well, as workers often skip necessary appointments, check-ups and treatment regimens for chronic conditions, which in turn puts their health at risk.

As coverage has grown in complexity over the past decade, it’s important that you provide the resources for your employees to choose the health plan that is best for them. Here are three tips that will help them get the most out of their benefits.

Don’t skimp on explaining

While some employees’ eyes are bound to gloss over while someone is explaining the various plan options, their networks, their copays, deductibles and more, it pays to take the time to explain them step by step.

That means breaking the benefits down to the basics in language anyone can understand. Avoid getting bogged down in health insurance jargon and keep it simple. The simpler the better.

Don’t think of it as talking down to your employees, because there’s a good chance some of them are not familiar with how health coverage works. Encourage questions, by telling them there are no stupid questions. Invite employees to speak one-on-one with your benefits point person if they have questions they’d rather ask privately.

Make benefits communications all year long

When the new year starts and open enrollment is in the mirror, most employers don’t reach out to staff until a few weeks before the next year’s enrollment period starts.

Plan now for regular benefits communications throughout next year. Send them e-mails and materials during the course of the year that remind them to consider how their current coverage is measuring up to their needs.

This is especially important if someone’s health situation changes. They may be looking to make a change during the next open enrollment, and feeding them periodic memos about their coverage can help them educate themselves and prepare.

Communications could include explainers about cafeteria plans, health savings accounts, how to use their health benefits wisely, and more.

Know your crew

After open enrollment, run a report looking at what plans your employees are signed up for and see if they are concentrated in certain plans. Many employees when choosing health plans ask their co-workers, which often leads to them choosing a plan that is not optimum for them since there are many factors that may vary, including:

Their age.

Whether or not they are married.

Whether or not they have children.

Their health situation.

That’s why it’s important to run some analytics on your employees’ health plan choices. We can work with you to make sure that they are in the right plans and identify what might be a better alternative for them.

For example, in many cases, the younger and healthier someone is, the best choice may be a high-deductible health plan with lower premiums, tied to an HSA. Older employees and those with health conditions — those who are more likely to use medical services and be on medication — may need a plan with a lower deductible.

The takeaway

It benefits both your employees and you if your employees are in the appropriate plan for their life and health situation.

Fortunately, you can ensure that they understand their benefits by understanding their needs and helping them learn about their benefits throughout the year.

As cancer rates rise among working adults, treatment has become one of the fastest-rising expenses in employer-sponsored health plans, according to a new survey.

The survey by the International Foundation of Employee Benefit Plans (IFEBP) found that 86% of employers have seen their cancer care spending increase over the past year, with a median rise of 11%, making it one of the most significant contributors to overall health care cost growth.

As more employees get diagnosed with cancer, which in turn increases the cost of care for employers, they are increasingly turning to strategies that direct plan members to high-quality, cost-efficient providers and care facilities.

What’s driving the trend

Employers report that cancer-related costs are increasing due to a mix of:

Expensive specialty drugs — Many of the newest cancer drugs can cost $20,000 to $40,000 per month, while gene and cell therapies can top $1 million per course. Even with negotiated network discounts, the compounding cost of these treatments is straining plan budgets.

New treatment technologies — New high-cost therapies like immunotherapies and gene-based treatments are regularly coming on line.

A higher number of working-age adults being diagnosed with cancer — New cancer diagnoses are expected to exceed 2 million cases in 2025, with rising rates among women under 50 and cancers such as colorectal, breast and cervical appearing more often in younger age groups.

More people are surviving cancer — Employees and their dependents are entering treatment phases earlier and remaining in survivorship programs longer, adding sustained costs for employers.

How employers are responding

Employers are increasingly turning to steerage techniques that direct plan members to high-quality, cost-efficient providers and care pathways. According to IFEBP, the most common approaches include:

Nurse navigators (63%) to help employees coordinate complex care.

Second-opinion programs (58%) to validate treatment plans.

Centers of excellence (42%), which offer bundled, value-based pricing.

Treatment center networks (24%) and virtual care clinic vendors (18%).

Value-based contracts (17%) and point-of-care testing (15%).

Among employers using these strategies, the primary goals are:

Improving outcomes (66%),

Offering personalized support (59%) and

Negotiating lower prices (33%).

Nearly a third is experimenting with alternative payment models such as shared-savings or bundled-rate arrangements that tie reimbursement to results rather than the volume of care.

Prevention and early detection

Experts say early detection offers the greatest potential to control both costs and outcomes. However, only about half of employees receive annual preventive care, and a significant portion of catastrophic cancer claims is linked to individuals who skipped routine screenings.

Employers can help by:

Promoting annual preventive exams and age-appropriate cancer screenings.

Covering or incentivizing genetic and biomarker testing for at-risk employees.

Incorporating AI-assisted diagnostics and at-home testing options for early detection.

Providing educational campaigns on modifiable risk factors such as smoking, obesity and inactivity.

To manage this, benefit professionals are urged to take a comprehensive, life-cycle approach from prevention and early screening to treatment navigation and survivorship care. As Julie Stich, IFEBP vice president of content, noted, employers must “offer the most effective cancer care treatments while also exploring cost-control techniques.”